Irish construction activity continues to rise, but at softest pace in eight months

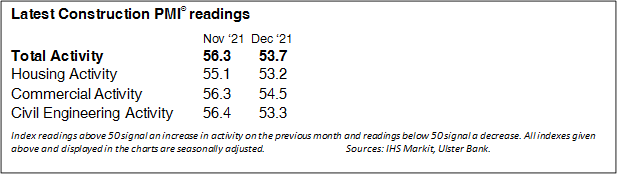

The Ulster Bank Construction Purchasing Managers’ Index® (PMI®) – a seasonally adjusted index designed to track changes in total construction activity – dropped to 53.7 in December, down from 56.3 in November. The reading signalled a further solid increase in activity in the sector, albeit the softest in the current eight-month sequence of expansion. Where activity rose, panellists generally linked this to improving client demand. Index readings above 50 signal an increase in activity on the previous month and readings below 50 signal a decrease.

Commenting on the survey, Simon Barry, Chief Economist Republic of Ireland at Ulster Bank, noted that: “Irish construction firms continued to experience solid growth in activity in December according to the latest results of the Ulster Bank Construction PMI survey. The headline PMI did ease back last month, but this is an unsurprising development following the signs of deceleration also contained in the Manufacturing and Services PMI survey results for December, which together indicate that high virus case numbers contributed to some moderation of Irish economic growth momentum at the end of the year. At 53.7, the headline Construction PMI still points to healthy growth in construction activity on a par with that experienced on average in 2019, while it also points to faster growth than signalled by the latest construction PMI for the wider Eurozone.

“While the late-year easing of momentum in construction growth bears close monitoring, particularly in the context of risks posed by still-very high case numbers, the December survey results nonetheless offered some encouraging signs regarding the sector’s prospects as we move through the early part of 2022. First, the input cost index fell for the second consecutive month, with a marked drop last month taking it to an 8-month low. While still at a very elevated level consistent with ongoing rapid increases in input costs, the readings at the end of last year do suggest that the intensity of cost pressures and related supply chain challenges is now easing somewhat. Second, construction firms continue to benefit from sharp ongoing increases (albeit at a slightly slower pace) in new orders amid reports of improving demand. And third, firms themselves remain confident about the coming year. Underpinned by strong pipelines of new work, expectations of further improvement in demand and confidence in housing market prospects, sentiment regarding the year-ahead outlook edged higher in December leaving it again well above the long-term average. Over 46% of firms expect their activity to rise in the coming 12 months – the highest reading since August.”

Widespread increases in activity

Growth of activity was broad-based in December, with all three monitored categories posting expansions. The fastest rise was in commercial activity where the rate of expansion was marked, albeit the softest in eight months. Solid rises were seen in housing and civil engineering.

Further sharp rise in new business

There were also signs of new order growth softening in December, but the rate of expansion remained sharp at the end of the year amid reports of improving demand and specific mentions of Health Service Executive (HSE) work having been secured. Where new orders eased, this was linked to the emergence of the Omicron variant of the COVID-19 pandemic.

Companies remain optimistic

Companies remained confident that activity will rise over the coming year, with sentiment ticking up from that seen in November. A strong pipeline of new work is set to support further improvements in new orders, while a number of firms signalled confidence in the housing sector.

Optimism in the outlook and increases in workloads meant that constructors continued to expand their staffing levels at a marked pace. Employment has now risen in nine successive months. That said, in line with the trends in activity and new orders, the rate of job creation eased.

Meanwhile, purchasing activity also rose at a softer pace. Where growth was recorded, this was linked to increasing demand and advanced purchasing to try and mitigate price rises.

The rate of input cost inflation remained elevated and was among the sharpest on record despite easing markedly from that seen in November. Higher costs for fuel, materials and transportation were reported, with firms also linking inflationary pressures to Brexit.

Brexit was also reportedly a factor behind longer suppliers’ delivery times, with shortages of materials and delivery drivers also contributing to delays. Lead times lengthened markedly again in December, albeit to the least extent since November 2020.